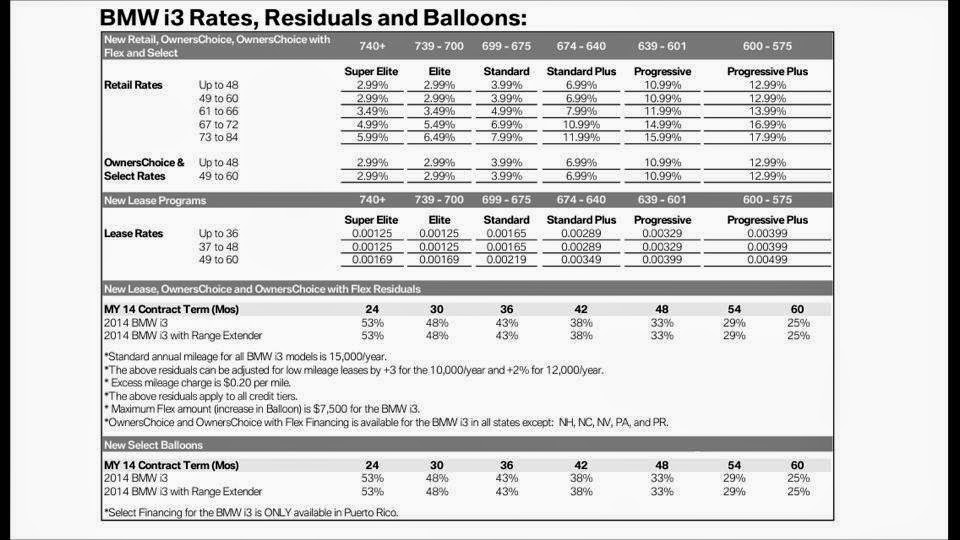

I bought the car on Saturday. My client advisor had agreed in advance to 2.74% APR with a large down payment, but when I got to the dealership and my client advisor brought me to the finance department, the first thing the finance guy said to me was that the 2.74% offer had been a mistake, that that was only available with traditional financing without a balloon payment, and that 2.99% was the lowest offer available for Owner's Choice. As proof of this, he showed me a printout of a spreadsheet showing a bunch of numbers for each BMW model. I noted that the chart was for 2015 model year cars and this was a 2014 i3, but he claimed the 2014s had the same numbers, which I have no way to verify.

The finance guy had also never heard of Owner's Choice with Flex (which is quite obviously listed on the BMW i financing page as one of the 3 available financing options, which any member of the finance team dealing with customers buying BMW i models should know backwards and forwards), leading me to further distrust anything he says.

He also was completely flummoxed by my request for a large down payment. I know leases and loans are typically used by people who don't want to pay for the entire car up front; those who do want to pay up front typically do so by just buying the car. But in my case I wanted to use Owner's Choice because it gives me the option of returning the car at the end of the term (in case EV technology has improved greatly by then and the value of the car then is less than the residual value). My client advisor had initially sent me options with $0 down and $3000 down, but I asked for an option with everything down (tax, title, license, fees, depreciation, interest) and no monthly payment, since I would save money by not having to pay the interest on that, and he complied and sent an offer PDF. But this had apparently not made it to the finance guy, and when I showed it to him, he was baffled as to why I wanted to do this, then unable to get his system to accept it. He called his manager, who was also baffled. BMW Financial Services was called 4 times. The manager went away, and was later consulted a second time. In the end I was allowed to make a down payment for everything except the interest, though even this was too much for their online system to handle and they had to use paper forms. Perhaps if I call BMWFS myself later I can prepay the interest as well and avoid paying interest on the interest. And perhaps, as i3atl said, I can ask them about the 2.74% APR. I had tried to call them before, but they basically would not tell me anything since I was not yet their customer.

![300W Car Power Inverter DC12V to AC110V,Dc to AC Car Plug Adapter Outlet with Multi USB[24W USB-C] /USB-Fast Charger(24W) Car Inverter,Car Charger for Laptop Vehicles Road Trip PISIFAU](https://m.media-amazon.com/images/I/41+ox0CwBYL._SL500_.jpg)

![[Updated] 600W Power Inverter for Vehicles 12v to 110v, Dual DC to AC Car Inverters Converter Car Adapter for Wall Plug Outlet with USB C 65w/24W Fast Charge for Laptop Road Trip/Long Drive/Camping](https://m.media-amazon.com/images/I/41+ce37YsRL._SL500_.jpg)